Advertisement

Advertisement

Italy: US Tariffs and Slow EU-fund Absorption Weaken Near-term Growth

By:

Italy’s economy is set to grow more slowly in 2025-26 given US tariffs and delays in recovery-plan investments. Still, reforms and continuing EU-fund deployment should support medium-term growth after 2026.

The Italian economy grew by 0.7% in 2023 and 2024, below its 1% medium-term potential and the euro-area average (0.9% in 2024). The economy has proven relatively resilient since the end of the Covid pandemic, benefiting from its large and diversified industrial base and export sector. Economic output is almost 5% above pre-pandemic levels, comparing favourably with that of other large EU economies such as France’s (+4%) and Germany’s (+0%), although weaker than the economies of Spain (+7%), Portugal (+9%) and the United States (+12%).

However, Italy is one of the most vulnerable countries in Europe to the potential consequences of a protracted trade war given its close trade relations with the US. The growing importance of the US as an export market for Italian manufacturers over the past five years has led to a substantial bilateral goods trade surplus, estimated at around EUR 39bn. Only Germany and Ireland have bigger goods surpluses with the US among euro-area countries.

Scope Ratings (Scope) estimates that a scenario involving US tariffs of 20% on EU goods imports and 125% on Chinese goods imports, plus retaliatory measures from China and, potentially, from the EU, could lower Italy’s economic growth by around 0.5-1pp of real GDP over 2025-27. The trade war would lead to slowdowns in industrial output, exports, and investment amid the heightened economic uncertainty.

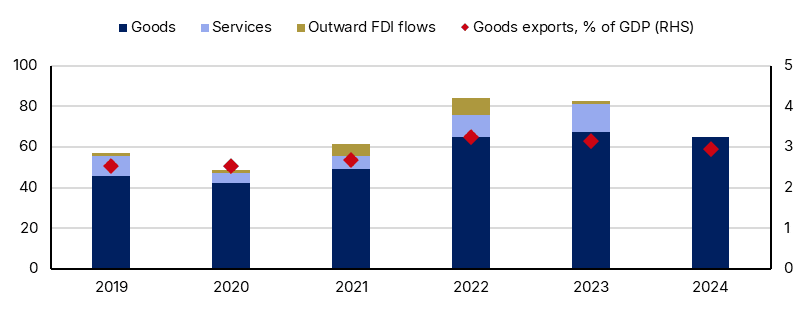

Italy’s goods exports to the US amounted to EUR 65bn in 2024 (10.4% of total exports, 3% of GDP), with 7% of Italian manufacturing production destined for the US market. Key export sectors to the US include pharmaceuticals, transportation equipment, automotives, machinery, and luxury goods. Italy also exported an average of EUR 10bn in services to the US between 2021 and 2023 and invested EUR 5bn in foreign direct investment (FDI) on average over the same period (Figure 1).

Figure 1. Italy’s buoyant exports to the US, 2019-24

EUR bn (LHS), % of GDP (RHS)

The full economic impact of tariffs on Italy remains uncertain, however, given the evolving US-EU trade regime and the heterogeneous elasticity of exports, which tends to be lower for patented pharmaceuticals but higher for cars, apparel, drinks and food except in high-priced luxury categories. Italy’s capacity to mitigate the adverse effects from US tariffs will also depend on its ability to diversify and access alternative export and import markets.

Recovery and Resilience Funds Should Support Growth Potential Despite Delays

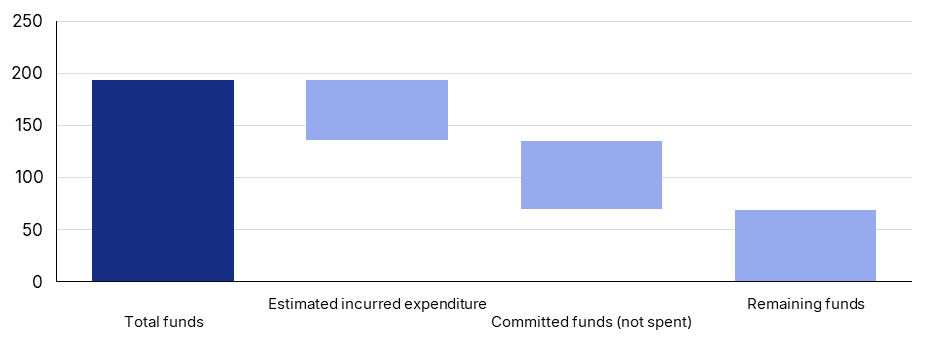

Given global trade tensions, Italy’s efficient deployment of EU recovery funds becomes even more important for sustaining domestic economic growth. Of the EUR 194.4bn allocated to Italy under the Facility, the country has so far received EUR 122.1bn, equivalent to 63% of the total allocated resources.

However, spending such a substantial sum has proven challenging, with estimated expenditure at EUR 58.6bn in October last year, about 30% of the total allocation according to Confindustria. Most resources to-date have been allocated for tax credits, railway construction and school infrastructure projects.

Lower-than-expected annual spending of allocated funds has also reduced the potential stimulus for the economy. In 2021, the government projected a cumulative impact of 2.4pp of additional real GDP growth for 2021-2024, which was revised to 1pp in 2024. Most of the economic stimulus is now expected in 2025-26, with an estimated cumulative impact of 2.7pp of additional real GDP growth. However, this implies exceptionally high expenditure of EUR 57.1bn in 2025 and EUR 49.5bn in 2026, which is unlikely.

With EUR 125bn (64% of total funds) allocated by implementing entities for the payment of contractors and service providers by the end of 2024 (Figure 2), that leaves about EUR 70bn to be allocated (remaining funds). Scope expects that by the end of 2026, most of the EUR 194.4bn will be allocated to projects that are then implemented in subsequent years.

Figure 2. Recovery and Resilience funds for Italy: an overview

EUR bn

The recovery plan’s capacity to stimulate Italian GDP growth will be spread over a longer period than initially projected. While not all funds can be spent by the end of the Next Generation EU programme, most should be committed to specific projects by then.

Finally, Italy’s growth potential of around 1% over the medium term should also be supported by structural reforms planned by 2026 related to the judicial system, competition law, public administration and procurement reforms, among others. These reforms and their impact on growth potential are critical to sustaining Italy’s high public debt burden, which stood at 135.3% of GDP at end-2024.

For a look at all of today’s economic events, check out our economic calendar.

Alessandra Poli is an Analyst in Sovereign and Public Sector ratings at Scope Ratings. Eiko Sievert, Senior Director in sovereign ratings and member of the Macroeconomic Council at Scope Ratings, contributed to drafting this article.

About the Author

Alessandra Policontributor

Alessandra Poli is an Analyst in Scope’s Sovereign and Public Sector ratings group, responsible for ratings and research on a number of public-sector borrowers.

Did you find this article useful?

Latest news and analysis

Advertisement