Advertisement

Advertisement

German Private Sector PMIs Flash Red; EUR/USD Dips on ECB Rate Cut Bets

By:

Key Points:

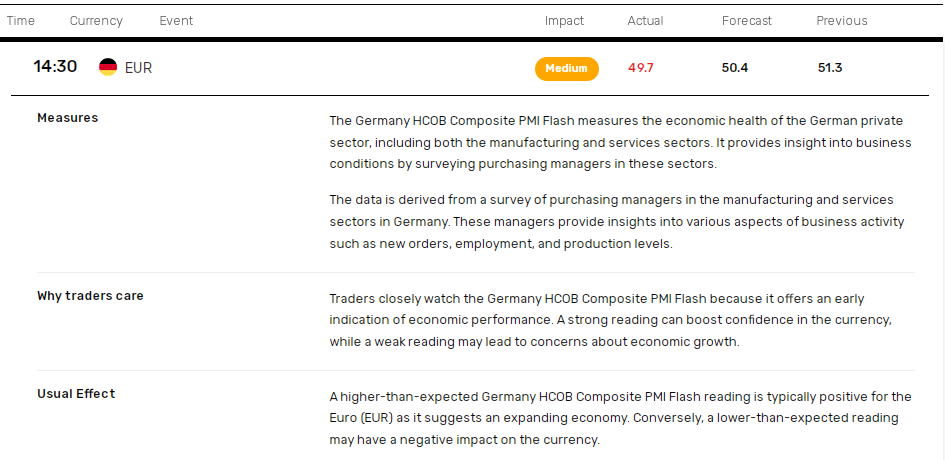

- Germany’s Composite PMI fell to 49.7 in April, signaling contraction and stoking fears of Eurozone stagnation.

- Services PMI dropped to 48.8, a 14-month low, with output prices rising at the weakest pace since October.

- EUR/USD slipped following weak PMI data, with investors weighing US-China trade de-escalation and EU tariff risks.

Germany’s Private Sector PMIs Flash Caution as Growth Outlook Dims

Germany’s private sector lost steam in April, reigniting fears of Eurozone stagnation as fresh PMI data and IMF downgrades darken the 2025 outlook. The HCOB Composite PMI dropped from 51.3 in March to a four-month low of 49.7 in April, indicating a marginal contraction.

The April PMI release echoed the IMF’s latest projections from Monday, April 21. The IMF expects Germany’s economy to stagnate in 2025 and expand by 0.9% in 2026, revising down forecasts by 0.3 and 0.2 percentage points, respectively.

Key signals from the April PMI survey included:

The HCOB Manufacturing PMI fell from 48.3 in March to 48.0 in April.

- Manufacturers reported a slight increase in orders, bolstered by overseas demand.

- Manufacturing sector sentiment weakened amid tariff concerns.

- Employment fell further across the manufacturing sector.

- Manufacturers reported a sharp fell in input prices, supported by a stronger EUR.

The HCOB Services PMI dropped to a 14-month low of 48.8 in April, down from 50.9 in March.

- Service providers reported a fall, citing economic and political uncertainty.

- Job creation across the services sector rose at the fastest pace since May 2024.

- The latest rise in services output prices was the weakest since October.

- Services sector sentiment dropped to the weakest since September 2023.

The data reflect easing demand conditions, supporting a more dovish outlook for the European Central Bank amid moderating inflation.

Expert Views on Germany’s Private Sector

Dr. Cyrus de la Ruble, Chief Economist at Hamburg Commercial Bank, remarked:

“US tariff policy has not caused a major slump in manufacturing just yet. In fact, manufacturers have managed to increase production for the second month in a row and even saw a slight uptick in export orders, something we have not seen since early 2022. This is pretty impressive and might be due to hopes of reaching some compromises with the US, along with Germany’s well-diversified export destinations – 90% of exports go to countries other than the US. Of course, there is still a lot of uncertainty, and optimism about future output has taken a bit of a hit.”

The Market Reaction to the PMI Numbers and Trade Developments

Financial markets responded swiftly to the PMI data. Before the PMI release, the DAX jumped to a pre-report high of 21,832 on optimism about easing US-China trade tensions. However, in response to the April PMI report, the Index briefly

On Wednesday, April 23, the Index was up 2.34% to 21,791 for the morning session. Hopes of a softer US stance on tariffs countered concerns about the German economy.

In the forex market, the PMI data weighed on EUR/USD, briefly climbing to a post-report high of $1.14085 before dropping to a low of $1.13912 On April 23, the EUR/USD traded 0.22% lower at $1.13945.

The EUR/USD pair remains sensitive to trade rhetoric and economic indicators. Rising trade tensions could fuel EUR inflows as a funding currency, while risk-on sentiment may drive EUR outflows, pressuring the EUR/USD.

Outlook Hinges on Trade Policy

On Tuesday, April 21, President Trump U-turned on China tariffs, declaring that levies will come down significantly from 145% but not to zero. A de-escalation in the US-China trade war may boost risk sentiment, potentially pressuring EUR/USD further.

However, US-EU trade developments will be crucial for near-term trends. A softer approach to EU tariffs would drive the DAX higher and weigh on the EUR. Conversely, a firmer stance on EU tariffs may pressure the DAX while boosting EUR demand.

Discover strategies to navigate this week’s market trends here.

About the Author

Bob Masonauthor

With over 28 years of experience in the financial industry, Bob has worked with various global rating agencies and multinational banks. Currently he is covering currencies, commodities, alternative asset classes and global equities, focusing mostly on European and Asian markets.

Did you find this article useful?

Latest news and analysis

Advertisement