Advertisement

Advertisement

Jobless Claims Fall, but Weak Manufacturing and Housing Data Disappoint

By:

Key Points:

- Philadelphia Fed index plunged to -26.4 in April—its lowest since 2023—signaling deepening factory sector weakness.

- U.S. housing starts fell 11.4% in March, with single-family starts down 14.2%, pointing to cooling construction demand.

- Despite economic softness, jobless claims declined to 215K, keeping the labor market outlook relatively stable.

Traders Weigh Weak Manufacturing and Housing Data as Jobless Claims Fall

U.S. macro data released Thursday offered a mixed view of economic momentum, with manufacturing activity sliding, housing starts tumbling, and jobless claims showing resilience—raising questions about the near-term policy path and its market implications.

Manufacturing Sentiment Slips Sharply

The Philadelphia Fed’s April Manufacturing Business Outlook Survey showed a significant deterioration in regional factory activity. The general activity index plummeted to -26.4, its lowest since April 2023, while new orders dropped to -34.2, marking their weakest reading since April 2020. Employment remained broadly steady, but the average workweek declined sharply. Notably, firms continued to report input price increases, with the prices paid index rising to 51.0, the highest since mid-2022. Selling prices also increased, as the prices received index edged up to 30.7, reinforcing inflationary cost pressures even as activity weakened.

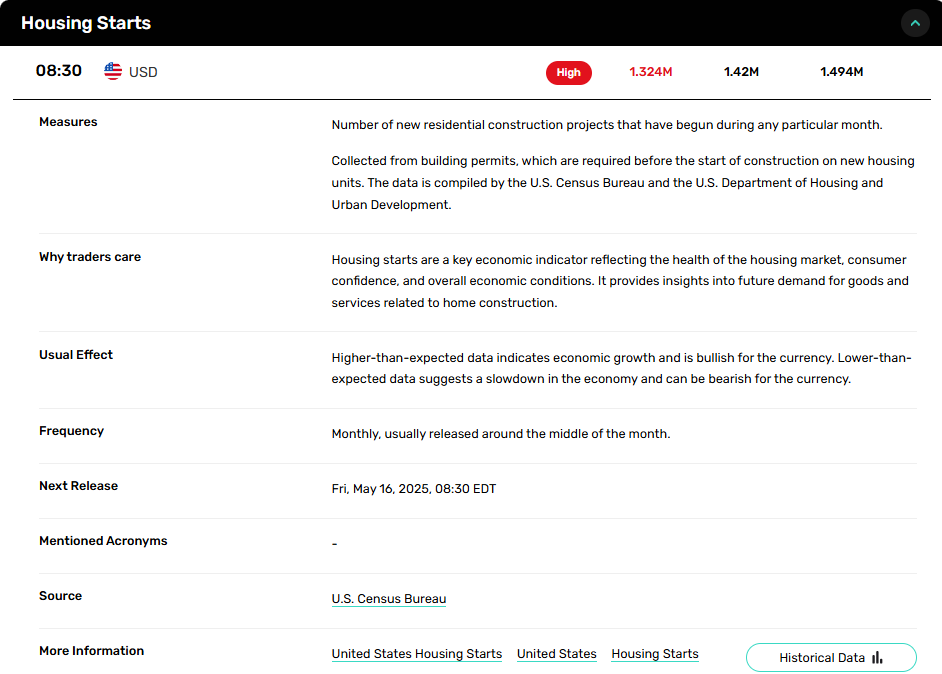

Housing Starts Contract Sharply in March

Residential construction showed signs of slowing. March housing starts fell 11.4% to a seasonally adjusted annual rate of 1.324 million, despite a modest 1.6% monthly gain in building permits. Single-family starts declined 14.2%, pointing to a pullback in new construction activity. Completions ticked down 2.1%, though still remained 3.9% higher year-over-year. The underlying weakness in single-family starts adds to concerns about housing demand in the face of elevated mortgage rates and softening builder sentiment.

Labor Market Remains Resilient

Offsetting the weaker housing and manufacturing prints, jobless claims data provided reassurance about the labor market. Initial unemployment claims fell by 9,000 to 215,000 for the week ending April 12, while the four-week moving average declined to 220,750. Continuing claims rose by 41,000 to 1.885 million, yet the insured unemployment rate held steady at 1.2%. This signals stability in labor market conditions, even as other sectors show signs of cooling.

Market Forecast: Cautious Bearish Bias

While labor market data remain firm, weakness in both manufacturing and housing points to a broader softening in economic activity. Rising input costs suggest inflation risks persist, which may complicate monetary policy expectations. The combination of deteriorating demand indicators with sticky price pressures could limit near-term upside for risk assets. Traders should brace for a cautious bearish tilt in equity and housing-related sectors, while keeping close attention on upcoming inflation and Fed commentary for further direction.

About the Author

James Hyerczykauthor

James Hyerczyk is a U.S. based seasoned technical analyst and educator with over 40 years of experience in market analysis and trading, specializing in chart patterns and price movement. He is the author of two books on technical analysis and has a background in both futures and stock markets.

Did you find this article useful?

Latest news and analysis

Advertisement